Three years ago when I was at the start of my credit repair journey, I obsessively tracked my FICO credit score using free apps like Credit Karma. I’d been on a hardship payment plan for my credit cards for over a year, and was eager to see my consistency pay off. I needed to apply for an apartment soon and wanted my credit score to be in as good of shape as it could be.

According to several credit trackers, I should be in good-enough shape for my renters application!

When the real estate agent called and said my credit pulled at 625 and I would need a guarantor,I was shocked. “That can’t be right,” I told her. “All the scores I’ve been seeing have been at least 670.”

“I don’t know what to tell you,” she said.

Turns out, there’s two different credit scoring models, the FICO and the VantageScore. So what’s the difference, and which one should you trust?

What is the FICO Score?

The FICO scoring model was introduced by the Fair Isaac Corporation in 1989 in an attempt to “democratize fair access to credit by helping to replace human judgment with a data-driven credit assessment.” In other words, the FICO score was created to take race, age, gender, and marital bias out of bank’s lending decisions. About 90% of top U.S. lenders still use the FICO scoring model when making lending decisions (Fortune).

In order to be eligible for a FICO score, your credit report must reflect:

- At least one credit or loan account older than 6 months

- At least one active account reported to the credit bureau within the past 6 months

- No indication that the account owner is deceased

Your FICO score is calculated based on five factors with varying weights:

- Payment history (35%)

- Amounts owed (30%)

- Age of credit (15%)

- New credit lines (10%)

- Credit mix (10%)

As of 2024, the most commonly used FICO score by lenders is the FICO 8. This is usually the score you will see reflected in your main credit report from Experian, Equifax, and Transunion.

There are also industry specific FICO scores, which combine the predictive power of the base FICO score “while also providing lenders a further-refined credit risk assessment tailored to the type of credit the consumer is seeking” (MyFico.com). If you’re planning to apply for a mortgage or auto-loan anytime soon, you should find out if your lender will be pulling your FICO 2, 4, 5, or other score. Below is a chart of the most commonly used FICO scoring models based on industry and credit bureau:

The FICO score ranges from 300-850 and uses the following categorization:

- Poor (300-579)

- Fair (580-669)

- Good (670-739)

- Very Good (740-799)

- Excellent (800-850)

The higher your score, the more likely it is that you will be approved for a credit line or loan, and the lower your interest rates.

You can obtain your base FICO score 8 for free at MyFico.com.

What is the VantageScore?

The VantageScore was launched in 2006 as a joint venture between the three main credit bureaus (Experian, Equifax, and Transunion) to compete with the FICO scores.

Whereas FICO requires at least 6 months of credit history to generate a score, the VantageScore can be calculated within one month after opening a credit line. This means that the Vantage scoring model can issue credit scores to 35 million people considered ‘unscorable’ by FICO (Fortune). For these reasons, along with the lower emphasis on

Your VantageScore is calculated based on six credit factors:

- Payment history (40%)

- Credit age and mix (21%)

- Credit utilization (20%)

- Amounts owed (11%)

- Recent credit activity (5%)

- Available credit (3%)

*Percentages based on VantageScore 3.0 model)

Unlike the FICO scoring model, which has different variations of scores for different kinds of lending, there’s only one VantageScore which gets updated every decade or so. As of right now, there is the VantageScore 3.0 model (launched in 2006) and the VantageScore 4.0 model (launched in 2017). VantageScore 4.0 is very close to 3.0, but emphasizes payment history and new credit activity more, and age of credit less Although VantageScore 4.0 is the newer model, the VantageScore 3.0 remains more commonly used by lenders and credit score estimators.

The VantageScore also ranges from 300-850 using the following categorization:

- Subprime (300-600)

- Near-prime (601-660)

- Prime (661-780)

- Superprime (781-850)

The Vantage scoring model is often considered more consumer friendly because it has a lower threshold for “Good” or “Prime” credit than the FICO model (661 vs 671). Additionally, both the Vantage 3.0 and the Vantage 4.0 ignore paid collections (including unpaid medical bills), whereas only the FICO 9 ignores paid collections accounts (Experian).

Which One Should You Trust?

The reality is, both the FICO and the VantageScore are legitimate scoring models, but the FICO scoring model remains the more popular score. If you’re planning to apply for a new credit card, auto or business loan, or mortgage, your lender will most likely pull one of your FICO scores.

This is important to know because many of today’s most popular and free credit-tracking apps such as CreditWise, Credit Karma and Credit Sesame will only display your VantageScore, which may not be the score your lender will see when making their decision.

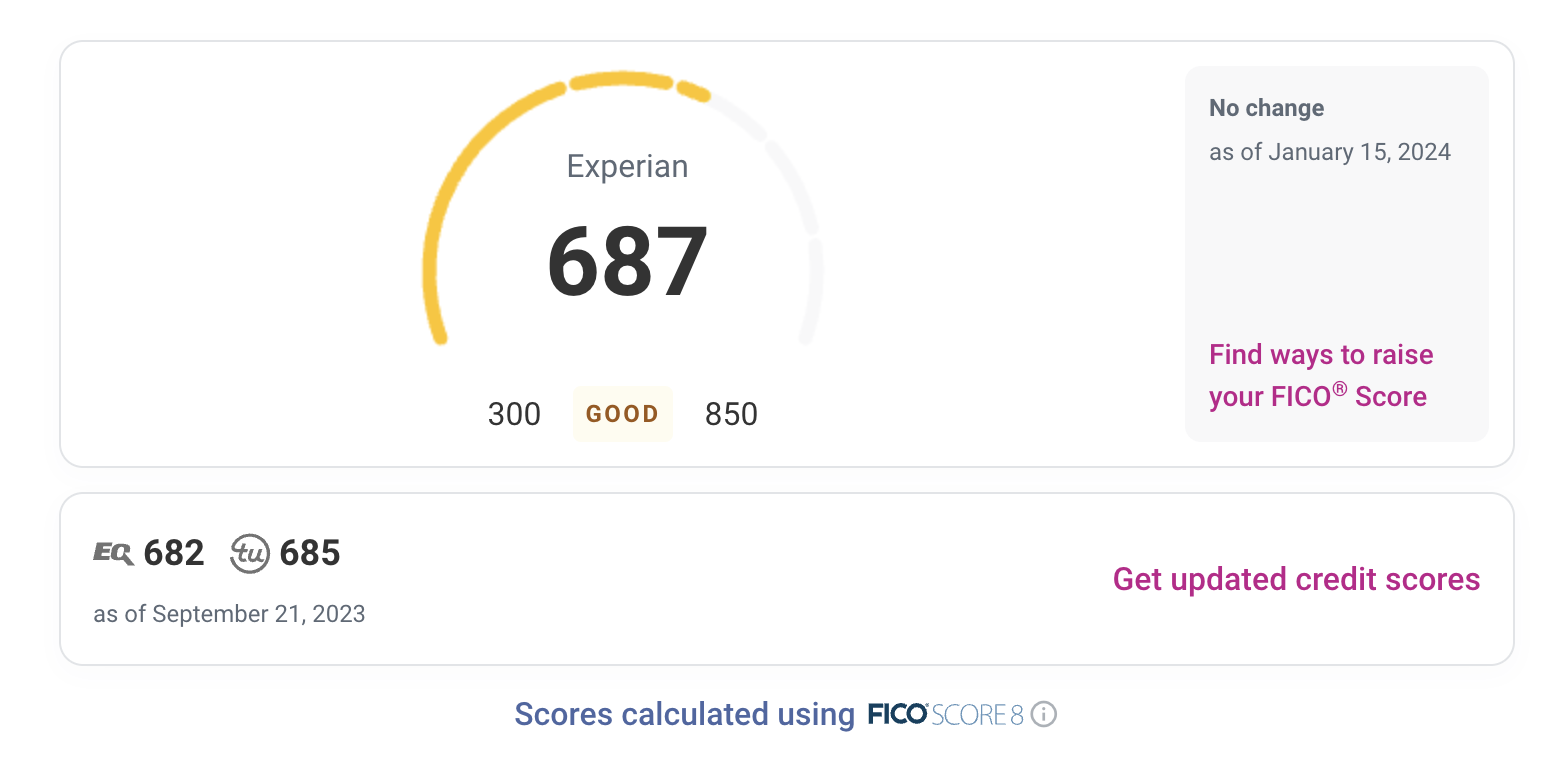

The good news is, it’s usually not hard to determine which scoring model your credit tracking app is using. For example, here is my credit score from the Experian dashboard, which clearly designates at the bottom that this in my FICO 8 score:

In contrast, here is a screenshot from my Chase CreditJourney estimator, which comes free if you have a credit card through Chase. As you can see in the lower right, this score was pulled using the Vantage 3 scoring model:

In this case, there was an over 70 point discrepancy between my Vantage and FICO 8 score due to some debt collections that were excused by Vantage but not by FICO.

Thankfully, I’ve been able to slowly repair my credit over the past three years that my score with both models is in the “Good” range now. That said, there was a time – like at the start of this essay – when this discrepancy was quite shocking, and forced me to change strategy. I hope this article can save you from the same unexpected surprise.

If you’re anticipating making any major financial moves in the future that will require a credit check – be it applying for an apartment, an auto-loan, or a mortgage – familiarize yourself with the credit bureau your lender uses and what credit model your lender will be using (or are likely to use). From there, you can find the appropriate place to pull your proper scores on your own.

If your scores as they stand are giving you panic, don’t despair. Check out how to significantly boost your credit scores within 6 months by becoming an authorized user and applying for a secured credit card.

Leave a Reply