I was $33,000 in debt by the time I turned 22.

This wasn’t the sympathetic, socially-justifiable student loan kind of debt.

This was $33,000 of credit card debt, accrued over a 9-month, blackout-style spending spree on clothing, farm-to-table dinners, bougie gym memberships, and Instagrammable getaways. The momentary thrill I enjoyed from all these purchases would evaporate with each new credit card statement. But I couldn’t stop.

My spending habits made no sense to me.

My childhood was perforated with painful memories of my parents fighting about money. My dad had a monstrous mountain of credit card debt, and my mom was hell bent on instilling me with money management advice, so I wouldn’t follow in my father’s footsteps.

But here I was: Twenty-two years old. New to New York city. Begging American Express to raise my credit limit, in hope of using that card to pay down another.

A single question haunted my mind:

“How the fuck did I end up like this?”

Since you’ve landed on this page, you might be asking yourself the same question about your finances.

If you’ve been caught in a cycle of self-sabotaging spending, uncovering your attachment style may offer some insights on why, and a pathway to healing. It did for me.

What is an Attachment Style?

I started working with a couples counselor to make sense of my messy love life, but the insights I gained about my attachment style helped me transform my (even messier) relationship with money.

Attachment theory is a psychological framework for helping people understand their needs, expectations, and patterns in relationships –much of which are shaped by our childhood experiences.

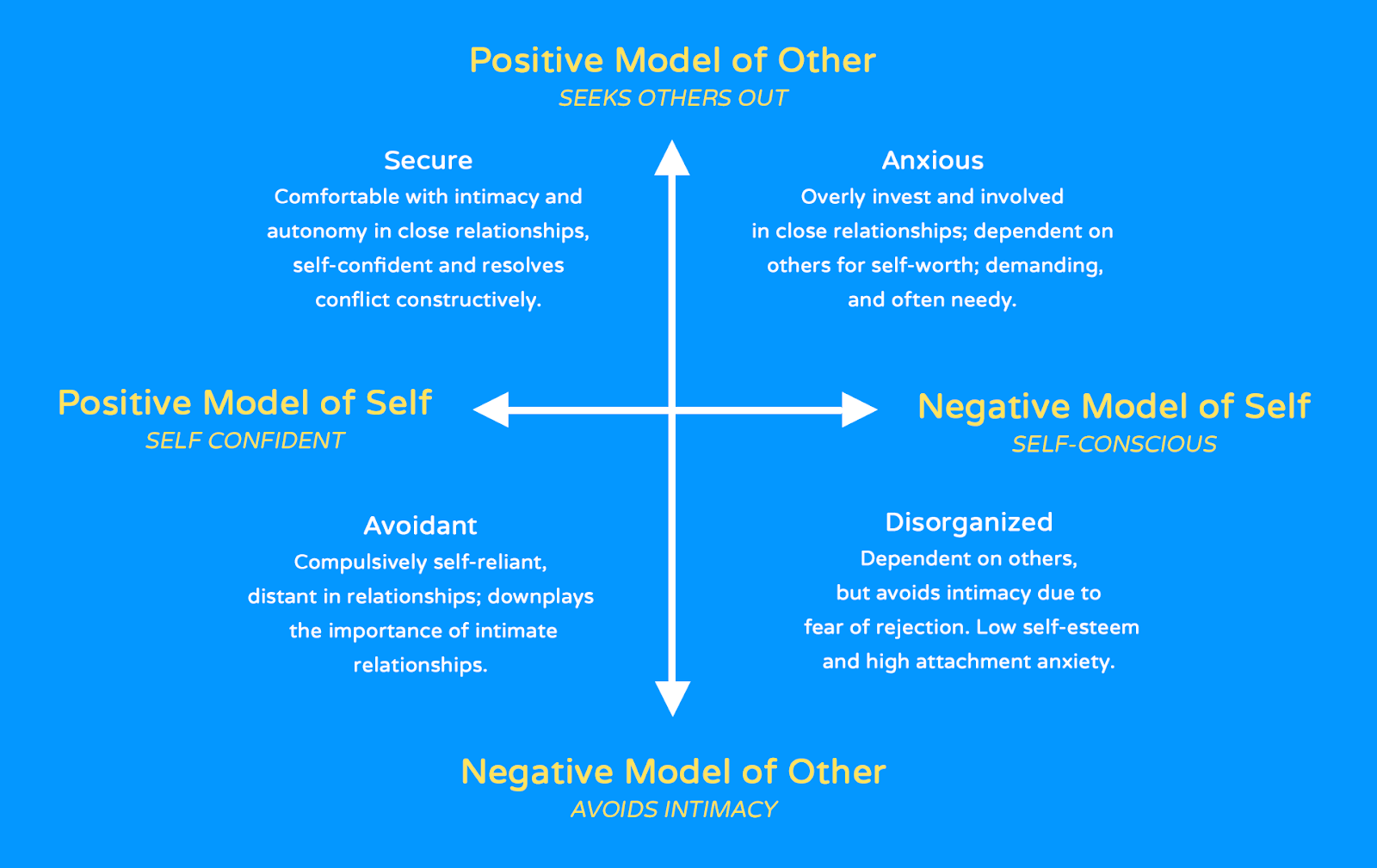

There are four attachment styles: secure, anxious, avoidant, and disorganized.

Source: Bartholomew’s two-dimensional model of attachment.

While these attachment frameworks were designed to describe our behavior in high-stakes romantic relationships, studies from Tilburg University and University of Arizona have found that your attachment style can impact your finances as much as your love life.

In particular, those with an anxious attachment style are particularly susceptible to engaging in irresponsible financial behaviors. As someone with an anxious attachment style, I can personally attest to this.

What is Anxious Attachment?

People with an anxious attachment style tend to be deeply self-conscious, and depend on others to feel good about themselves.

At our best, anxiously attached people are highly perceptive, thoughtful, and caring. But when we’re stressed, we’re consumed by our insecurities, fear of abandonment, and will go to great lengths for validation.

These behaviors usually stem from a childhood where emotional support was inconsistent, leaving us with two take-aways: others cannot be trusted and we’re not good enough as we are.

How My Anxious Attachment Led to My Debt Crisis

In the same way I thought the right partner would absolve me of all my insecurities, I thought money would do the same.

But at 22, I didn’t have much money. I had an inconsistent gig as a freelancer, three credit cards, and a chip on my shoulder.

In retrospect, there were three ways my anxious attachment kicked in and seeped into my spending habits.

Compulsive Spending

I was haunted by a constant sense of inadequacy. I didn’t feel smart enough to be hired for a stable job. I didn’t feel fashionable or fit enough to be considered attractive . I didn’t feel spontaneous and interesting enough to be worthy of friendship.

I thought if I could buy the right things, my insecurities would diminish. Credit cards enabled me to buy the status symbols I craved, fast. But none of those purchases boosted my self-confidence.

Instead, I found myself in an endless cycle of buying more stuff, reveling in an all-too-brief dopamine high, and then finding something more that was missing, and upping the ante.

Running from Reality

In relationships, anxiously attached people often minimize their own needs, in hope of holding onto a partner. I did the same with my finances: sacrificing my long-term stability for momentary relief.

Because my confidence depended on spending money I didn’t have, my credit card statements were astronomical. It got to the point where I couldn’t make the minimum payments. But I also wasn’t ready to part with my lavish lifestyle. So I took an “ignorance is bliss” approach, and just stopped checking and paying the balances all together.

This strategy preserved my self-esteem in the short term, but destroyed my inner-confidence and credit score in the long run.

Overworking and Risky Behavior

Eventually, my creditors closed my cards, and debt collectors started calling.

I needed to find additional ways to pay off my balances and bankroll my life. So I entered an era of workaholism: taking on every side gig I could find, working eighteen hour days, and getting into risky, get-rich-quick schemes.

I was doing my best to re-establish financial security and build-back my savings. But then there were moments where digging myself out of debt felt like such a lost cause that I’d relapse, and impulsively blow what little money I’d saved.

How to Heal Your Anxious Attachment

Psychologist Nicole LePera makes the point that “We don’t do compulsive behaviors because we lack willpower. We do them because it’s the only way we know how to self-soothe. Soothing is an instinctual behavior, not a moral one.”

Whether it’s in relationships, or with money, everybody has the power to move from an anxious attachment to a secure attachment. To do this, we have to learn new, more sustainable ways to self-soothe.

Below are four strategies I’ve used to finally wean off my anxious behaviors, get out of debt, and develop a more secure relationship with money:

Identify your worth

Because anxious behaviors are often triggered by low self-esteem, it’s imperative to find new sources of confidence outside of your money and possessions.

My therapist had me journal my own life story, paying attention to any skills, accomplishments, and empathy-building experiences that emerged. I kept a sticky note of those qualities on my bathroom mirror as a reminder of what I can contribute to the world. When feelings of self-doubt and insecurity came up, which they inevitably did, I’d pause and force myself to go back to that list.

This exercise also ties in well to the next step.

Insert space between your thoughts and actions

When we’re feeling triggered and unsure of ourselves, there’s an urgent desire to make that feeling go away. This can lead to those impulsive purchases I talked about earlier, which feel nice in the moment, but make our financial anxiety and trust worse in the long run.

One of the most important things an anxious attached person can do is learn to recognize and validate their feelings, without necessarily acting on them.

I start my day with 10 minutes of sitting still and noticing what’s floating around in my head. Some might call this meditation. I just call it sitting still and paying attention. I follow that with 10 minutes of journaling, just to get those thoughts out of my head.

If I’m having a self-critical thought, I look at my shortlist of strengths and remind myself of all the other things I am besides my insecurities.

If I’m having an urge to buy something, I ask myself, “What’s the worst case scenario if I don’t get this thing right now? What would my life look like without it?”

Debtors Anonymous is a free and non-judgemental space to learn these skills in community and find accountability partners.

Tell your friends

Speaking of accountability partners, another way to build your self-esteem is to be honest with close friends about your financial situation, and your desire to live more simply.

It can be humbling and scary, but I’ve found that talking with my friends about my need to cut back on expensive dinners, shopping, and trips has always been met with support.

Sometimes, that candor even opened the door for my friends to share that they were financially struggling as well, and we were able to support each other.

Get a clear picture of your finances

Against all my ego-protecting instincts, I forced myself to review my financial accounts and take an honest look at my expenses, income, debts, and assets.

This can be an anxiety inducing process, but there is peace to be found in clarity.

Once I knew what I was working with, I challenged myself to live below my means. That sentence sounds more fun and adventurous than it felt in the moment. But facing your life head on is something you’ll be proud of in the long run – and it will, in fact, make for an epic story.

If you’re like me and your anxious impulses led you into debt or credit crises, I encourage you to connect with a credit counselor.

I’m biased, but I personally recommend booking a free call with our founder Michael (you can do that directly below), who can help you learn about debt settlement options, lower your monthly credit payments, and repair your credit score.

After a year of working with him, I no longer have debt collectors calling me everyday, am enjoying the benefits of a high credit score, and can finally say I have a secure attachment with money.

Leave a Reply